BLAST Pension Strategy

Addressing Pensions Without Pension Obligation Bonds

What is an Unfunded Accrued Liability?

An Unfunded Accrued Liability (UAL) is the shortfall between pension benefits earned by city employees and the funds set aside to pay those benefits through the California Public Employees’ Retirement System (CalPERS). Upland’s UAL grew for years, mainly because CalPERS investments underperformed long-term expectations.

All participating cities must make annual fixed payments to CalPERS to pay down their UAL. These payments are based on the CalPERS discount rate. The UAL is like a loan balance, and the discount rate is like the annual interest rate. In June 2020, the City commissioned an actuarial report that found Upland’s UAL was $127 million. The CalPERS discount rate at the time was 7%. To pay off this UAL, the City would have had to make $228 million in payments to CalPERS over the next 22 years.

What Steps Has the City Taken to address its UAL?

Upland’s City Council and staff have long been aware of the funding challenges posed by the City’s UAL and have taken proactive steps to address them.

- In 2016, the City established a Section 115 Pension Trust (the Pension Trust), a special account that sets aside and invests monies restricted to meeting the City’s UAL. The City made five deposits into the Pension Trust totaling $12.4 million. Establishing this trust protects taxpayer resources by ensuring pension obligations do not divert funds from essential public services, shielding general services from future pension shocks.

- In 2016, the City approved Memoranda of Understanding (MOUs) with City labor groups, requiring employees to contribute to the City's share of pension costs. Safety employees contributed 3%, and non-safety employees hired after January 1, 2020, contributed 1.4%. While this did not reduce the existing UAL, it would help prevent further unchecked growth.

- In November 2016, the City decided to transfer fire service operations to San Bernardino County, effective July 2017, to reduce anticipated future pension liabilities.

- In 2020, the City retained Urban Futures, Inc. (UFI) to advise the Finance Committee and City Council on Upland’s UAL challenge.

- Between September 2020 and December 2021, the City held multiple public workshops, meetings, and study sessions to fully explore the UAL and develop solutions, including the issuance of Pension Obligation Bonds and other alternative strategies.

- In 2021, the City adopted a Pension Funding Policy and General Fund Reserve Policy calling for accelerating the payoff of new UAL bases.

What are Pension Obligation Bonds?

Some cities met their UAL obligations by issuing Pension Obligation Bonds (POBs). These bonds raise a lump sum of cash that is immediately used to reduce or eliminate a UAL. This creates a liability at a stable, fixed rate but comes with legal and investment risks and a loss of flexibility. In 2021, due to concerns over these risks, the City decided to pursue other alternatives.

What is the BLAST Strategy?

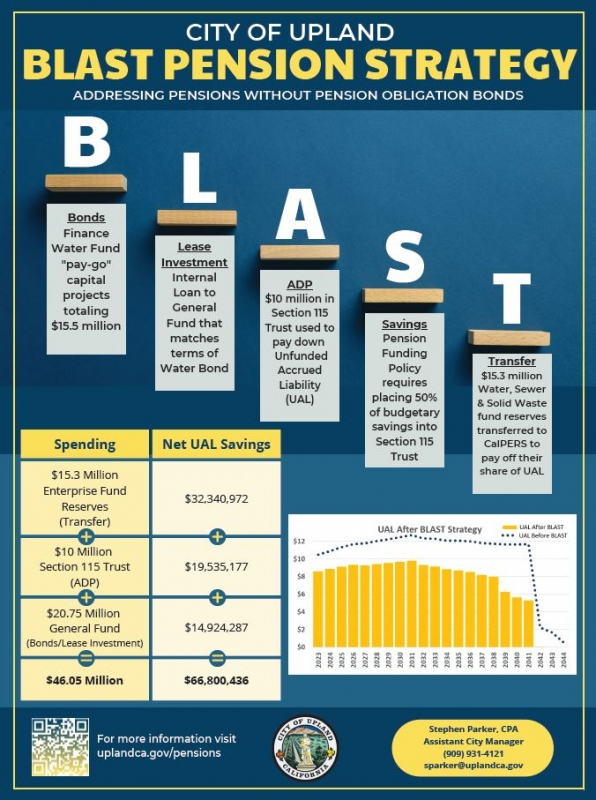

The BLAST strategy is projected to save the City an estimated $66.8 million in UAL payments over the next 22 years, using only the City’s current cash reserves and a fiscally disciplined approach. BLAST is a coordinated initiative to immediately reduce the City’s UAL by combining existing reserves with low-interest loans and replacing CalPERS's 7% discount rate with a 2% internal loan rate. The strategy also revises the reserve policy to boost Pension Trust savings for potential future pension obligations. The BLAST strategy has five key components:

| ADDITIONAL DISCRETIONARY PAYMENT (ADP) - The City made an ADP of $10 million from its Pension Trust to pay down the UAL. Early paydowns reduce the UAL base, lowering future implied interest and total payments. This is estimated to save a net of $19.5 million toward the City’s UAL. |

|

What Has Been the Effect of BLAST?

The City Council approved the strategy, and implementation began in December 2021. BLAST was completed in 120 days by spring 2022. The BLAST strategy will save the City an estimated $66.8 million in UAL payments over the next 22 years. This is an annual savings of $3-4 million in the City’s UAL payment obligation.

The BLAST strategy enabled Upland to proactively reduce pension liabilities, mitigate future cost increases, and enhance long-term financial stability. Through these targeted actions, the City maintains its ability to deliver essential services while meeting pension obligations in a fiscally responsible way.

City of Upland’s BLAST Pension Strategy

Addressing Pensions Without Pension Obligation Bonds

Addressing Pensions Without Pension Obligation Bonds

Upland City Council and Staff have been aware of and have taken steps to address the City’s rising pension costs and its unfunded accrued liabilities (UAL) with the California Public Employees’ Retirement System (“CalPERS”) for a number of years.

UAL - The unfunded accrued liability is the measure of the funding shortfall of each agency’s pension liability. The UAL is equal to the difference between:

- Estimated value of benefits earned and expected to be paid to current employees and retirees in the future in today’s dollars; and

- Market value of investment held by CalPERS.

The City’s UAL as of its most recent actuarial report (June 30, 2020) is equal to $127 million. The city is required to make annual fixed dollar payments to pay down its UAL. UAL payment are calculated based on CalPERS discount rate of 7.0%, with payments totaling over $228 million over the next 22 years.

Some of the steps City Council has taken to address its UAL include:

- Establishing a Section 115 Pension Trust with PARS in 2016 to set aside and invest monies restricted to addressing the City’s pension liability.

- Making 5 subsequent deposits into Section 115 Pension Trust totaling $12.4 million.

- Approving Memorandum of Understandings with all safety labor groups in 2016 calling for safety employees to begin contributing 3% towards the employer portion of the CalPERS normal cost (on top of the entire 9% employee share).

- Deciding in November 2016 to transfer City fire service operations to San Bernardino County (transfer took place in July 2017) in part to limit and/or reduce anticipated future pension liabilities.

- Approving Memorandum of Understandings with all non-safety labor groups in 2019 calling for all classic non-safety employees hired after January 1, 2020, to begin contributing 1.4% toward the employer portion of the CalPERS normal cost (on top of the entire 8% employee share).

- Issuing an RFQ in 2020 soliciting municipal advisors, culminating in engaging Urban Futures, Inc. (“UFI”) to provide pension advisory services to assist the Finance Committee and City Council with evaluating Pension Obligation Bonds and other options.

- Adopting a Pension Funding Policy and General Fund Reserve Policy in 2021 that established three approaches to set aside funds with the City’s Section 115 Pension Trust and called for accelerating the payoff of new UAL bases.

- Holding 10 public workshops, meetings and study sessions with the Finance Committee and City Council from September 2020 to December 2021 to understand its liability and evaluate its options.

Due to legal constraints and concerns about market timing risk, the City decided to pursue alternatives to Pension Obligation Bonds. Working with its financial advisor, it developed multiple strategies to address its UAL.

Due to legal constraints and concerns about market timing risk, the City decided to pursue alternatives to Pension Obligation Bonds. Working with its financial advisor, it developed multiple strategies to address its UAL.

The key to the BLAST Strategy is tapping into underutilized resources, primarily excess reserves in the City’s Water, Sewer & Solid Waste funds, which had a 12% share of the UAL ($15.3 million).

There are 5 component parts to the BLAST strategy:

- Bonds – Issue tax-exempt bonds to finance “pay-go” capital projects. Tax-exempt bond rates are much lower than the CalPERS Discount Rate (2.0% vs. 7.0%). The Water Fund issued $15.75 million of 15-year bonds @ 92% for proceeds of $15.50 million.

Issuing bonds for capital projects enable the Water Fund to utilize its previously designated reserves to make investment in or internal loan to the General Fund.

Issuing bonds for capital projects enable the Water Fund to utilize its previously designated reserves to make investment in or internal loan to the General Fund.

- Lease Investment – The Water Fund used available reserves to make an internal loan to the General Fund to pay a portion of its UAL. The loan, which took the form of investing in General Fund debt, matched the terms of the Water Bonds ($15.75 million / 15-years @ 1.92%). The Sewer Fund also made a $5 million investment with the General Fund from its available reserves at the same rate.

- ADP – The City made an Additional Discretionary Payment (ADP) from monies held in the Section 115 Pension Trust to “pre-pay” $10 million of its UAL – saving $19.6 million in total UAL payments.

Savings – The City Council adopted a formal Pension Funding Policy, which requires 50% of budgetary savings realized from the BLAST strategy to be deposited into the Section 115 Pension Trust, which will be available to address future increases to the UAL.

Savings – The City Council adopted a formal Pension Funding Policy, which requires 50% of budgetary savings realized from the BLAST strategy to be deposited into the Section 115 Pension Trust, which will be available to address future increases to the UAL.- Transfer – The Water, Sewer & Solid Waste fund reserves transferred $15.3 million from its reserves to CalPERS to pay off their share (12.9%) of the City’s UAL.

After City Council approval, implementation of the strategy commenced in December 2021 and was complete by the Spring of 2022 - taking 120 days to complete. The BLAST Strategy will save the city $66.8 million in UAL payments over the next 22 years, and lowering its annual UAL payment by $3-4 million, all without the use of taxable Pension Obligation Bonds (POBs).

For more information about the BLAST Strategy, contact:

Julio F. Morales

Kosmont Financial Services

Senior Managing Director

jmorales@kosmont.com

626-298-9583

Documents sorted by SEQ in Ascending Order within category